Pension Planning Hack #1 – The Trick to the Payout

Welcome to the first part of our pension planning series, where we use our pension planning hacks and our expert knowledge to tell you how to get the most out of your Pillar 3a - and how you can benefit from it with volt 3a.

At some point in time, after years of paying into your Pillar 3a you will want to pay out your pension assets. As you probably know, this withdrawal - usually several hundred thousand francs on average - is subject to tax. But did you know that you can already do something today to optimize these taxes for your payout later on and save money in the process? Welcome to the first of our pension planning hacks, where we show you how to get the most out of your retirement savings, and how volt 3a helps you to apply them.

One of the most prominent arguments in favor of pension planning with pillar 3a is the tax advantage when you make deposits. As an employee with a pension fund, you can pay in up to CHF 6,883 per year into your pillar 3a and can deduct it from your taxable income when you file your tax return. This reduces your tax burden and you save tax every year, which helps you to achieve your pension goal faster.

If you are not connected to a pension fund, it is even possible to pay up to 20% of your net income up to a maximum of CHF 34,416 into Pillar 3a.

The bill comes last

Although you save tax every year with your annual Pillar 3a payment, you have to pay a portion back to the tax authorities – even if at a lower, privileged rate. Exactly how high this tax rate is depends on various factors, including the amount of your pension assets paid in by then and your canton of residence. In principle, the higher your pension assets, the higher the taxation. With direct federal tax, taxation is progressive up to a certain level. However, there are major differences in taxation models at cantonal level.

Progressive taxation for pillar 3a pension assets

Breaking the tax progression

Our pension-planning hack takes effect at the tax progression. In order to keep this as low as possible, we recommend the following measure, in which volt-3a customers receive full support: Open several 3a custody accounts and distribute your pension assets equally among different accounts. In volt 3a, you can open up to 5 accounts at the same time with just one click. Depending on the overall situation, you can then arrange to close these individual accounts one by one over a period of several years - starting earliest at 60 for men and 59 for women. The tax is then calculated individually for each year and on the basis of each closed custody account, which means that the progression (for the federal government or depending on the canton) is lower overall compared to closing all accounts simultaneously. You can thus save several thousand francs in taxes. How about an example?

Meet Peter and Anna

The example of Peter and Anna, both residing in Zurich, clearly shows the advantage of staggered payment of several custody accounts over several tax periods.

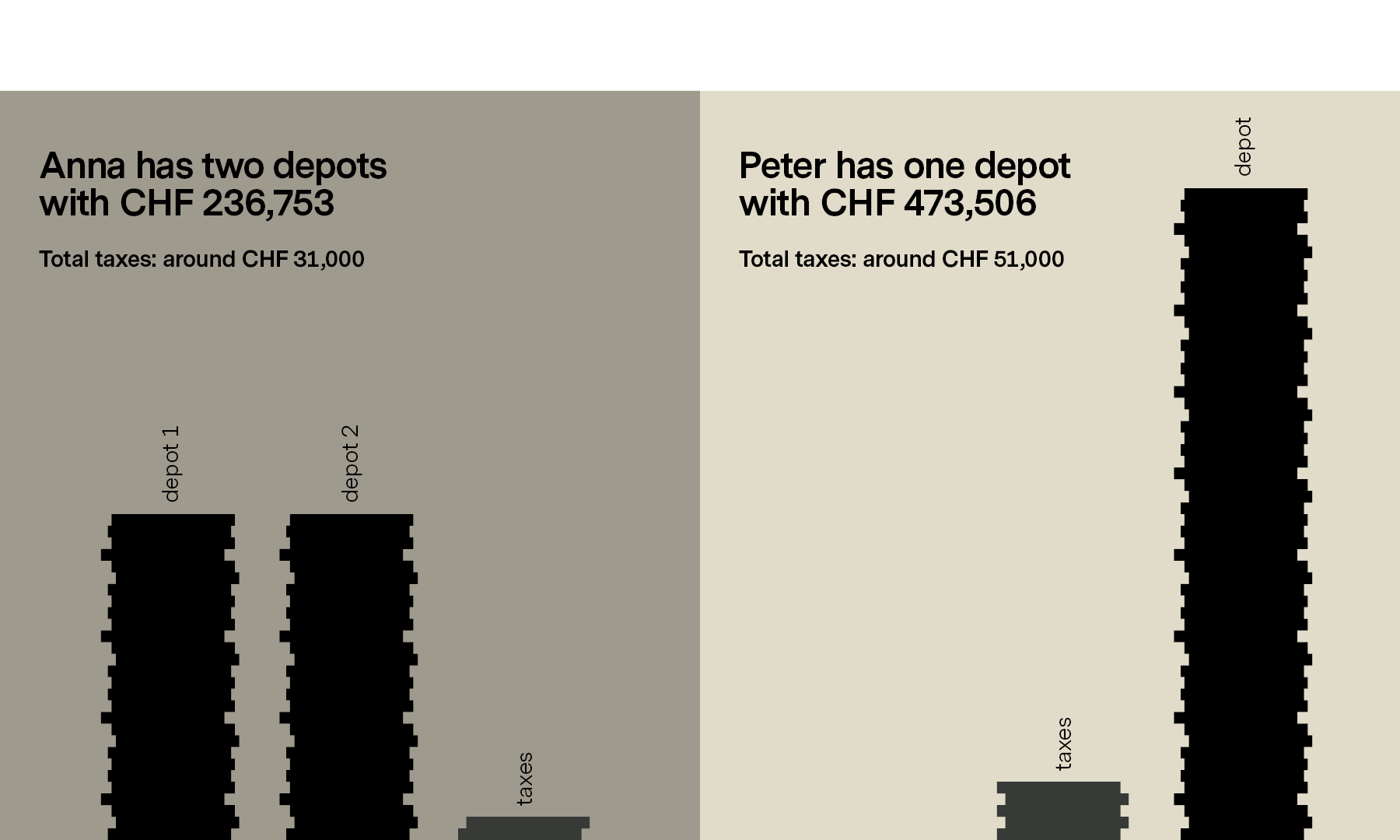

Peter pays out his saved pension assets of CHF 473,506 at the age of 65 at the beginning of his retirement. The Zurich resident will pay a total of around CHF 51,000 in taxes - these will go to the federal government, the canton and the municipality.

Anna also has a total of CHF 473,506 in pension assets - but unlike Peter, she has divided this amount between two accounts, which she opened a long time ago. Each of them contains a credit balance of CHF 236,753, which she can pay out in two different years. The result: Anna's tax burden for her overall capital withdrawal is only about CHF 31'000 - even though she lives in the same community.

This means that Anna's savings are over CHF 20'000 higher than Peter's, all thanks to the staggered payment of pension assets from several accounts, distributed over different years.

How many depots make sense?

How many deposits are useful, or over what period of time one should withdraw the money depends on the personal situation. With our volt 3a digital pension planning solution, you not only benefit from Vontobel's concentrated investment expertise, you also receive recommendations and optimization proposals on precisely such questions. And best of all: When you open volt 3a, we take care of the transfer of your existing pension assets for you, if you wish.

Tobias Vinzent

Head of Wealth Planning

Tobias Vinzent runs the Wealth Planning department with various expert teams in financial and pension planning, estate and tax planning as well as foundations and accounting. He passed the examination to become a federally certified SME financial expert and certified financial planner. Tobias Vinzent also has a CAS in applied psychology and a Master’s in Advanced Studies in Swiss Finance (concentration: Wealth Management).

Legal Disclaimer

A product of the Vontobel 3a Vorsorgestiftung and Bank Vontobel AG. The document is expressly not intended for persons who, due to their nationality or place of residence, are not permitted access to such information under local law. This publication is marketing material,

is provided for information purposes only, and does not take into account individual needs, investment targets, or financial circumstances. The publication does not constitute an offer, a solicitation, or a recommendation to use the Vontobel service described in it, to purchase or sell securities or other financial instruments, or to take part in an investment strategy. Capital expenditures in financial products and markets pose various risks (e.g. market, currency, or liquidity risks). Before making an investment decision, investors should

obtain personal advice from their financial and tax advisor concerning the risks associated with the investment and their personal situation. The content, scope, and prices of the services and products described in this publication are governed exclusively by the agreement concluded with the individual investor. Bank Vontobel AG and Vontobel 3a Vorsorgestiftung decline all liability for losses arising from the use of this publication. Further information is available at volt.vontobel.com